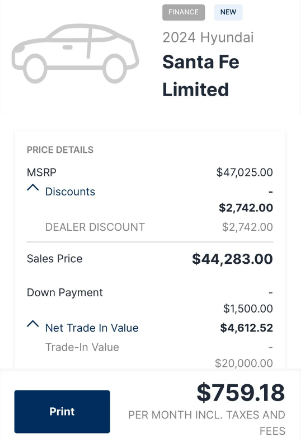

I’ve been eyeing the Santa Fe for a while, and with the current discounts on the ’24 models, I’ve been considering trading in my ’22 Tucson Hybrid for the ’24 Limited in Rockwood Green with the grey interior. The trade-in offer for my Tucson is below my payoff, so I’d be rolling that into the new financing. Do you think it’s better to go for it now or wait until next month to see if finance rates improve, even if that means losing the discount on the ’24s? I also received an offer on an XRT for $39,878 (MSRP $42,720), which would put me at $671/month with the same terms as the Limited. Any advice?

If you’re at $759.18 a month for 84 months, that’s pretty steep. You’re looking at around 12k in interest alone. Not sure this is worth it, especially if you’re rolling over from another loan.

Maybe just stick with what you have and avoid adding more debt. No need to switch cars every two years if it means you’ll be upside down on a loan.

Blake said: @Orion

Good points. I’m currently at $465 a month for 72 months on my Tucson, just put down equity from my old CRV.

Your current payment is almost half what you’d be paying with the Santa Fe. Maybe take that $300 difference and put it in a high-interest savings account until you can pay down enough to trade up without going into deep debt.

If you can’t manage a 60-month term, it’s probably better to hold off. Ideally, aim for 36-48 months on car loans.

Blake said: @Orion

Good points. I’m currently at $465 a month for 72 months on my Tucson, just put down equity from my old CRV.

If you can’t afford a 48-month term or shorter, then it’s probably too much. The 20/4/10 rule or 20/3/8 is helpful: down payment / years of finance / max percent of income for monthly payments.

Why upgrade from a 2022 to a 2024? It’s just not a good financial move. If you’ve got extra cash, use it to pay down the Tucson loan early instead of jumping into a new one.

Thanks for all the advice. Deal’s off for now, and I’m planning to save that extra $300 per month to pay down the Tucson so I’m not upside down. Then I’ll reassess next year if rates drop.

You want to roll over $4,612 in negative equity on a car over $44k and only put down $1,500? That means nearly $64k for a $44k car… maybe look at something more affordable like a 2009 Civic.

Honestly, sounds like a bad idea. Do you really need to swap out the Tucson? If you map this all out, you’ll probably see that the losses on the Tucson plus the high interest make this a poor financial choice.

If you’re insistent, maybe hold off until December when deals tend to improve. Plus, use sites like the Hyundai website to find models and offers in your area, and reach out directly to dealerships to see what fees they’ll tack on. Shop around and don’t settle for dealer markups and junk fees. Trust me, going in prepared can save you a lot.

TLDR - Think twice, and if you go for it, negotiate hard. It’s your money!

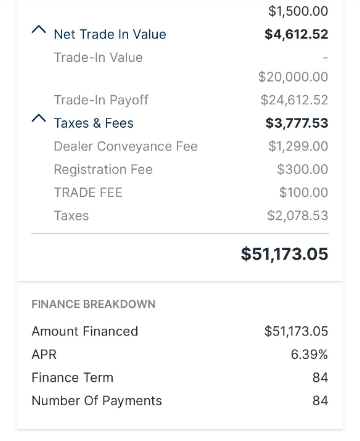

Dealer fee, trade fee… they’re just extra costs. You’re looking at $1,400 in unnecessary fees. I’d suggest finding a different dealership when you’re ready.

You’re setting yourself up for a long loan and might still be upside down. I used to sell cars, and 84-month loans rarely make sense unless you’re desperate. Don’t overextend yourself—get something you can afford with 15% down or at least a trade-in that’s paid off.